'A business(economy) that makes nothing but money is a poor kind of buinsess' – Henry Ford

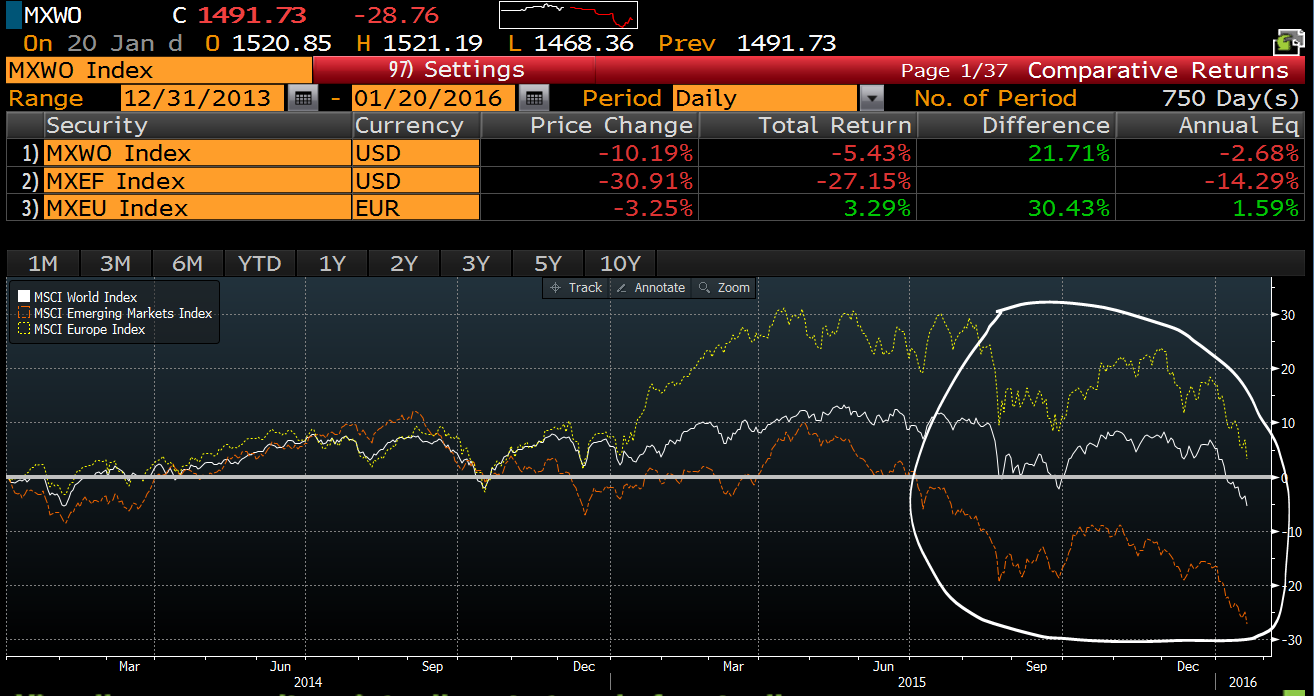

What a start to the year! In the space of three weeks we have lost all of the gains in the stock market from 2014 and 2015.

The chart below is MSCI World, MSCI Emerging markets and MSCI Europe – the picture is the same for US, Japan and China. A wasted two years of "lower for longer?"…. .absolutely!

https://pbs.twimg.com/media/CZPEgXQWIAEEVo5.png:large

{kind=link}

Meanwhile Italy is on the brink of a new banking crisis, Portugals new government is about to reverse all of the gains made over last five years and UK is getting pushed towards the exit door for EU – add to this the major political issue of refugees, an US election which on behalf of sanity is going from bad to terrible – and a Middle East imploding from low oil prices.

Yes, it's a tough start to the year and to my confusion pundits and strategist's a like continues to look to China for excuses. China is the easy scape goat, but seriously if anyone is surprised about China growth slow-down and its needs to buy time for changing its economic mix-up they need their school money back…..!

To explain the mechanics of the present correction which is now entering a bear phase I have done this illustration – The three drivers of markets (Main market focus)

Note: The cycle axis or velocity is the US$ - (Higher US$ slower speed, weaker higher speed)

There are three major drivers of markets:

Fed rate cycle, being the dominant central bank of the world it dictates absolute direction of global rates. The hike in December came after a big increase in funding costs for the corporate and private sector, but now policy rates (central banks) and market rates is aligned and projected higher.

The price of money is always the most important input to any economy and right now market is pricing 1.7 hikes in 2016 (42.5 bps) and Fed is promising 3-4 hikes (75/100 bps)

When focus again returns to Fed and its rate cycle it will be a game of 'who blinks first?' – The Fed backing down or market moving up?

For now, clearly market continues to fade and distrust Fed's intensions.

Oil prices, everything you have done today and everything you will do for the rest of the day will have electricity consumption in it. Oil is still main generator of car fuel and electricity so the input cost of energy is key determinant for real wages and real consumption.

Oil has negatively affected both the price of money and growth globally. Price of money through less "slush money" – the Middle East and all the commodity producers no longer runs surplus' on their current accounts and hence they have less money to invest in US and Europe fixed income markets. This drives up the price of money and academic studies have shown that the net reduction in yield when 'slush money' is flowing freely has been roughly 100 bps. (I.e.: Long-term bond yields would have been 100 bps higher in this cycle if not for these investors)

Likewise growth impulses from commodity market countries has been net negative due to less money to import capital goods and services.

Oil and energy prices however also have upward drive to growth. Europe will in 2016 feel the full impact of lower energy prices as a net energy importer it stands to make considerable gains in disposable income at consumer and business level. This will make it difficult for ECB to be keep printing money throughout 2016.

ECB, however, is always lagging the real world (Do not forget in early 2014 Draghi dispelled any notion of deflation!) – so ECB will move aggressively, but doing so they will have ignored the fundamental net positive impact from energy and the overall healing of the consumer and business sector in Europe. Conclusion: ECB will be on pause by this summer and central banks will again be facing in the same direction…

China, that GDP is coming is hardly any surprise!

Furthermore, the West continues to see and analyse China based on balance sheet assumptions. This is creating serious wrong conclusions. Does China have issues? Absolutely! Will China have a hard landing? Maybe, but unlikely. Will China then see soft landing? No, that is unlikely, but they will have a "long landing". Meaning they have enough private savings to keep the game going add to this the Silk Road, the internalisation of the RMB and the AIIB bank. This is not how a collapse looks like. China is structurally slowing down, but Chinese tourists will spend 275 bln. US$ overseas this year and the new China export is tourists and soon money.

The "devaluation" is more of a test drive of free capital movements and a support for economy through raising liquidity to finance debt servicing. That China is finally again moving forward with more free capital movement and facilitating credit for finance hungry emerging markets countries is hard for me to interpret as a net negative and major focus point!

What is interesting is how aggressively the market is using China as an excuse – it is best shown by this customer survey by BAML:

Get this! Since the last survey (November) Fed has hiked policy rates, but the market is has moved its focus from the Fed rate cycle to China in a big way:

In November 59% of those surveyed saw Fed as the biggest macro theme, now less than 23% feels it important! China meanwhile has moved from 27% to 66%!

Conclusion

The market continues to only be able to focus on one-risk at a time. 2016 so far has been about China – the "only" real concern though should be the disparity between where Fed sees the rate cycle in 2016 (3-4 hikes) and the market (1.7 hikes). How that evolves is the next directional move in macro.

The weak data start will not get Fed to step off the pedal in January, but as data starts to come in for January I fully expect Fed to back to down to first 2-3 hikes, then 1-2, and even ultimately 0-1 but for now, we are involved in a Mexican standoff.

Strategy

We came very negative into Q1 as our "Mind the gap" Q1 Outlook also projected, but we are getting to levels where "value" again is materialising, especially in tired credit spectrum (investment grade and above) and energy/materials.

My model is 100% risk off, but I am now hedging with CALL options on equity upside and my strategy is more and more….short on the day - closed by end of day awaiting new information. (Rotation back to Fed being main focus)

My US$ call – weaker in 2016- is close to being initiated. The long-term momentum is turning slowly. (I will keep you posted on when it turns).

That is still the main conclusion: The US$ direction is still the King, the gasoline of the market. The higher the trade weighted US$ goes the less risk assets will return. The path of least resistance for investors, policy makers and world growth remains the same: We need a weaker US dollar.

Safe travels,

Steen Jakobsen

Chief Investment Officer, Saxo Bank AS

This email may contain confidential and/or privileged information.

If you are not the intended recipient (or have received this email

by mistake), please notify the sender immediately and destroy this

email. Any unauthorised copying, disclosure or distribution of the

material in this email is strictly prohibited.

Email transmission security and error-free status cannot be guaranteed

as information could be intercepted, corrupted, destroyed, delayed,

incomplete, or contain viruses. The sender therefore does not accept

liability for any errors or omissions in the contents of this message

which may arise as a result of email transmission.

Ingen kommentarer:

Send en kommentar